EXECUTIVE SUMMARY: The $5.45 price USDA projected for corn in the September WASDE report is an outlier relative to the marketing year data for the last 10 years, meaning it takes a major shift in demand structure to justify the projection. The only other apparent shift was in the 2001/2007 period when ethanol went from no measured use to 5.0 bb. There have been higher projected prices, but those are all associated with smaller supply estimates. The article is not about whether the price estimate is right or wrong. If the demand has shifted, expect a new era of prices. If the demand has not shifted, better consider locking in some prices.

This post is in reply to questions received after the Monthly Corn Demand, 2017-2021 post in a marketing discussion group. “Do you have anything like this for 2006-2014? I wonder if we would see similar outliers.”

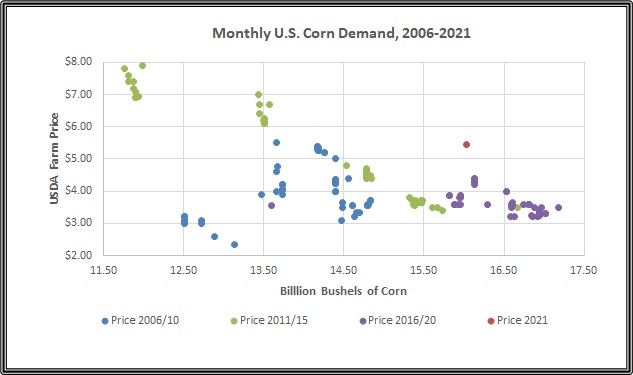

In a short reply, I indicated that I didn’t have the information, and then I decided the questions were worth spending time to put the data together. The chart is a plot of USDA monthly price estimates against total supply for the September to August marketing year. In addition to the original question, I was interested if a time shift could be picked up by grouping the data.

I am sure everyone will see different things in the chart, but here is my take. The blue dots at or below 13.0 bb are all from 2006, and I had mentioned earlier that I thought the data supported a conclusion that there had been a demand shift as we moved into 2007 and later years. There has not been a price estimate below $3.00 in the last 15 years with more than 13.20 bb. The addition of ethanol to the domestic use line, and a ramp up from zero recorded bushels used in 2001 to more than 3.0 bb in 2007 goes a long way to satisfy my curiosity for the issue.

There is a lot of volatility in the rest of the 2006/10 series, but very few outliers. Changes in supply estimates explain a huge portion of the variation. If you will give me a pass, on that set for now, I think the story is in the 2011/15 (green) and 2016/20 (purple) data. If you accept that the demand curve for corn is not linear, it is pretty easy to fit a curve down through the green and purple data that has no major outliers for 10 years. The purple points above $4.00 and 16.0 bb are at the end of the 2020/21 marketing year and reflect the rationing that took place when consumers had delayed buying as the price rallied and ended up having to bite the bullet. It is a form of demand shift. There was NOT 16.0 bb available at the end of the marketing year, or even 1.0 bb of stocks. No one is sure yet what the stock numbers were/are so pent up demand met a limited supply. But now the pipelines are filling with another projected supply of 16.0 bb.

The most conspicuous outlier is the one red dot for the September 2021 projection above $5.40. Please note and consider that there has not been any other time in the last 15 years that USDA projected a monthly average price above $5.00 with a supply of 14.5 bb or more. So, the answer to the original question is that there has not been an outliers like the new projections for 2021/22 any time in the last 10 years.

For demand to shift, there must be change in consumers’ preferences. The feed category has been relatively stable with most of the fluctuation in the quantity demanded explained by price, livestock inventory, etc. USDA is not projecting any increase for 2021/22. Food and seed without ethanol has been very constant. Ethanol use has fluctuated, but most of the variation has been related to demand for oil, and anything on the upside is not encouraging. USDA is not projecting an increase in the Food category, and ending stocks are considered a residual. That leads me to the conclusion that the only source of demand increase will be through international demand, and USDA is not projecting an increase in exports. If you are buying into the higher prices for 2021/22, I am respectfully asking (no it is a plea) if you will share your insight into where the “demand increase” implied by the $5.40 plus projections is coming from. Thank you.

Posted by Keith D. Rogers on 27 September 2021